Owing to , Experian, TransUnion and you will Equifax gives all of the You.S. consumers 100 % free weekly credit history owing to AnnualCreditReport so you can include debt wellness in abrupt and unprecedented difficulty due to COVID-19.

In this article:

- What is actually a produced Domestic?

- Gurus of getting a produced Home

- Cons of shopping for a made Family

- Could you Score a loan to own a produced Household?

- Are a created House Good for you?

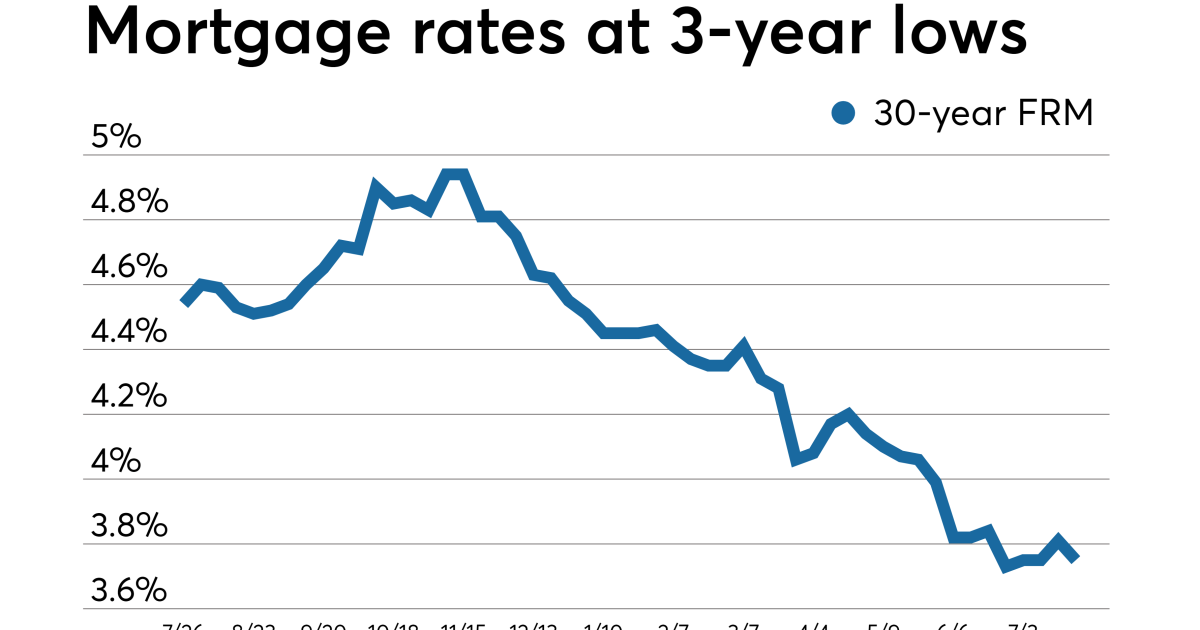

The average cost of a new household about U.S. reached $five hundred,100 in the , according to the Federal Reserve loans Spruce Pine. It offers some create-become property owners considering a less expensive alternative: are created residential property, that your Are created Houses Institute estimates so you can pricing an average of $87,000.

Are made homes can be produced significantly more inexpensively as they are have a tendency to mass-built in industrial facilities then gone in one destination to various other. Before buying a made home, however, you will know their benefits and drawbacks, resource choices and prospective a lot more costs.

What’s a produced Household?

Are formulated belongings have been in existence for a while, nevertheless You.S. Agencies regarding Casing and you may Metropolitan Advancement (HUD) didn’t initiate controlling them up to 1976. One factory-based home-built just after Summer 15, 1976, that suits HUD construction and you will coverage guidelines is a manufactured home. Factory-situated land created before 1976 are generally named mobile residential property, whether or not one identity often is utilized interchangeably with are designed land.

Are made home need to be constructed on a wheeled chassis you to definitely gets eliminated in the event the residence is transferred to their permanent site. This distinguishes her or him away from modular belongings, which can be and additionally factory-founded, but are manufactured in sections and you can come up with towards a long-term basis during the family web site. A created house could be used yourself house otherwise on the rented end up in a made family community.

Today’s are formulated land usually are difficult to differentiate of an usually built household. You might pick from a number of floors arrangements and you may incorporate decks, garages and decks. Has actually are priced between timber-burning fireplaces, salon bathrooms and you may high-end kitchen areas.

Advantages of getting a made Home

- Economy: An average of, were created house cost $57 each sqft, as compared to $119 for every single legs for new traditionally depending house. Are manufactured house meet HUD conditions for energy efficiency, cutting electric costs, as well.

- Production price: Cellular home are made inside the a manufacturing plant to help you consistent HUD standards. In lieu of generally dependent house, framework are not delay by inclement weather or difficulties with zoning and it allows.

- Mobility: If you want to disperse, you are capable bring your were created home along which have you.

- Use of business: Certain are formulated domestic parks offer usage of features such as for instance pools, recreation bed room otherwise on the-website gyms.

Drawbacks of getting a made Home

A manufactured family with the a permanent base on your own property can also be getting categorized since the real property and you will funded with a home loan. You could potentially financing precisely the domestic otherwise the domestic and you may the brand new home it uses up.

However, are manufactured homes with the hired residential property, such mobile home parks, are believed private possessions and must feel funded having good chattel loan. Chattel finance are acclimatized to finance movable gizmos, such tractors otherwise bulldozers; the device (the home in cases like this) functions as security. Chattel money will often have higher interest rates and you will limited individual defenses weighed against mortgages. Personal loans, which can be used the objective, can also finance a created domestic. Such as chattel funds, unsecured loans usually have high rates than just mortgage loans.

Are created house that will be classified as houses and you may meet specific most other requirements meet the requirements to own mortgage loans due to Fannie mae and Freddie Mac computer. They may along with qualify for are made home loans supported by the new Experts Management, U.S. Institution off Farming and you will Reasonable Homes Administration (FHA). The fresh FHA actually guarantees home loans for are designed property classified once the private possessions.

The credit score must fund a manufactured family varies created into bank, the borrowed funds size and the value of the fresh new security. Generally, however, it’s much harder to invest in are created homes than traditional home. A study because of the Individual Finance Cover Bureau located fewer than 30% out of are created home loan applications try accepted, compared to over 70% off loan applications getting web site-established house.

In advance of financial support a created home, score a duplicate of your credit report off all the three biggest credit agencies in the AnnualCreditReport. Look at the credit rating or take procedures to alter their score if necessary, such as for instance providing late membership latest and settling loans. Definitely look around and evaluate your loan options before making the decision.

Was a manufactured Domestic Right for you?

A made domestic is a reasonable homeownership choice, however it is important to acknowledge the risks. You have so much more choices for investment a made household for folks who very own or get home to accommodate it. If you intend to help you book room from inside the a cellular family playground, ensure you know debt financial obligation and then have book arrangements on paper.